16 Dec 2024

Post by Midwest Money Mentor

I’m sure, if I ask a room of 100 people “Who here loves to budget?”, we would get like 99 hands that excitedly raise up, right? Everyone loves to budget, which is why I am so excited to write about this topic.

Back to realty. The paragraph above was sarcastic, in case you couldn’t tell. Financial educators don’t want to write about budgeting because people don’t want to learn about budgeting. Everyone knows they should budget, but even just hearing the word “budget” makes people’s faces scrunch up into an “Eww, gross.” face.

I’m sure there are tons of reasons this general reaction comes about, but the truth of the matter is, if you do not budget (even if just loosely), you are very unlikely to get ahead financially. Budgeting allows you to control your money. LET ME REPEAT THIS – Budgeting allows you to control your money. If you do not budget, at least loosely, you do not have control over your money. If you have no idea how much you are spending, then you are likely spending wildly and without purpose. And this may shock you (sarcasm again), but if you don’t control how much of your money is getting invested, saved, used for debt payoff, etc. then you will likely not save, invest, or pay off debt to get out of debt. BOOM! Crazy huh?

Another mind blower (final sarcasm paragraph, I swear), if you spend all of your money, you cannot build wealth. And apparently, you need to build wealth to not have to work until you die. I’m saying some really hard to believe things here, some would say shocking, so feel free to take a moment to think about all of this (ending of the total sarcasm bombs).

So, for real now, it would be great if you went hard-core on your budgeting. It would be great if you looked at your spending every day (like people use to when they used check books). It would be great if you made sure the first thing that came out of your paycheck (even before taxes and health insurance) went to your designated investments so you could freaking retire some day (freaking A!). And it would be great if you put specific dollar amounts as the only amounts you can spend in certain areas (like eating out and fun). But we understand that is not going to be everyone (or even most people in America).

But you can still put in minimal effort so you at least know if you are consistently spending less than you make and building wealth (which is the whole point of budgeting). What we are going to do (below) is give you some different ways to attempt to budget, just in case you do have the motivation to be diligent and want to really, truly, control your wealth building. Secret note, I really, really, really want you to budget in some way or else very little that is taught in these posts and classes will help as much as they could.

While giving you some different ways to budget, I am going to give you a slacker option that at least gets you consistently paying attention to what your income and spending look like on a monthly basis. If you see a trend where your expenses are more than your income (or close to your income), you can choose to jump in to your spending and see what you can cut. Remember, the goal is to spend 80% or less of what you make so you can invest 20% or more of your income and actually build wealth (worst case. If you want to retire early, you will likely need to invest a higher percentage of your income). I know you will not, likely, be investing 20% or more right away, but we need to get you there over time.

Here are some of the budgeting techniques we will discuss for you to try out:

- Zero-Based Budgeting.

- Needs/Wants/Investment Budgeting.

- Lazy/slacker option.

Numero Uno – Zero Based Budgeting –

Zero based budgeting is a very detailed budgeting in which every dollar of income you receive is assigned a job. At the beginning of the month you have zero dollars set to remain idle. This budgeting direction takes the most work, but is by far the option that will give you the most consistency with your spending. It really is very similar to what your parents or grandparents did with their checkbooks. Every expenditure was documented in the check book and each person (who used it correctly) knew how much money they had available to spend or invest or save. And the smart ones saved and invested first, then spent the rest.

This budgeting type has been highlighted as the best choice for budgeting by well known persons in finance, such as Dave Ramsey – Click Here For His Website. And one could argue it likely is the best because the person using this budget format is not leaving any dollars to waste AND that person has to be fairly involved in the tracking of spending in order to use it correctly. The more time you spend monitoring/tracking your money, the more likely you are to focus on using your money efficiently. Consistency builds habits and the more consistent you are at looking at your expenses the more likely you are to improve what you are using your money for.

If you are just starting out with budgeting, or you are someone who really needs to change your spending habits quickly, I would recommend using this budget option. You DO NOT have to use it forever if it turns out you do not enjoy this technique. But, it will get you understanding where your expenses are truly going each month more quickly than other approaches. So, even if you use this budgeting technique for 1 year, you will likely be better for it.

How does it work? First you should download the last 6 months of bank statements from all bank accounts you spend out of and review what spending you regularly have. No, it does not have to be 6 months, but many people have semi-annual expenses, such as holidays and birthdays, that pop up and looking at the last 3 months may not catch many of those. You then break up this spending into specific categories. Examples of categories would be mortgage/rent, car payments, car insurance, vehicle gasoline, groceries, dinning out, subscriptions, pet food/car, haircuts/health/beauty, fun, insurance, and more. You also want a category for investments, savings, and miscellaneous. Miscellaneous, because random things will pop up and having a certain amount of your income planned out for these random expenses will help make sure your budget does not get totally derailed.

After these categories are broken out, you either can download a budgeting app online, or even through Dave Ramsey’s site, or use an excel spreadsheet to plug in these categories and the corresponding amounts of spending you want to go to each. Just a reminder, before you plug in your spending amounts, you first have to plug in the amount you need to go to investing, savings, or extra debt pay down (beyond the minimum payments). EVERY BUDGET YOU CREATE HAS TO BE SET UP WITH YOU INVESTING FIRST AND THEN LIVING OFF EVERYTHING YOU HAVE LEFT. Saving, paying off debt faster, and investing are NON-NEGOTIABLE budget line items! Make sure your brain knows that going in.

Quote time – Warren Buffett – “Do not save what is left after spending, but spend what is left after saving,”.

You likely will not get the amount that should be planned for each category perfect for quite some time. So, do not worry about being wrong a little bit with your initial budgeted amounts. Each month you can tweak your dollar amounts per category. Once you set up your expenses, investing, and savings category, you log into your bank account every day or every week (PUT IT ON THE CALENDAR AS A REMINDER) moving forward and plug into the app or your spreadsheet each expenditure and the dollar amount in each category. This allows you to see how quickly or slowly each category is filling up and if you need to change your habits/plans.

Review the total at the end of each month (also put that in your calendar along with other items to review). After a number of months, you will see what you need to adjust in order to reach your goals. Keep doing this activity each week and month and you will improve your personal financial understanding quickly.

Numero Dos – Needs/Wants/Investments

This type of budget, often also called the 50/30/20 budget, is more of a budget outline. In theory, using this style of budget, you would allocate 50% of your monthly income to basic needs such as food, housing, and other necessities. You would allocate 30% of your monthly income to wants and fun. And then you would have 20% of your monthly income allocated to savings/investments (just remember, the amounts for saving and investments needs to be the priority and come out first).

As mentioned above, you would want to still look at your last 6 months of bank statements to review your spending practices, and then lump those expenditures into these three categories. Each month, you would plan out your spending to match these total ranges and then weekly (or daily) monitor your expenses so you can make sure everything does stay in range.

This budget is much more relaxed than the zero-based budget and may people find they enjoy it more. The negative to this option, also, is that it is much more relaxed. And since you are not tracking each dollar to the same degree, it is easier to not have a true grip on your spending. If you are moderately good at managing your spending already, this may be a great fit for you as you may not need as much structure. If you historically have issues with spending and need better guard rails to keep you on the road to financial success, it would be better to start with the zero-based budget until you have your impulses reigned in (or just stay with the zero-based budget forever).

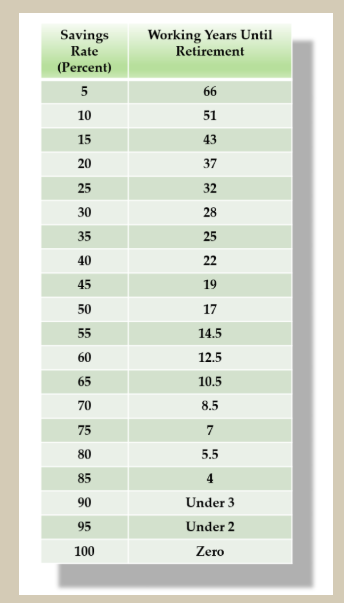

A side note with this budget option is that it is flexible. If you find that this budget direction is a better fit for you, but you want to be more aggressive with your saving and investing percentages, feel free to change the set up around. Many people in the F.I.R.E community, for instance, have their budget more around 40/20/40 or even 35/15/50, meaning they put 40% (in the 40/20/40 budget) or 50% (in the 35/15/50 budget) of their income towards investments. This speeds up their ability to retire early by a huge amount. For instance, theoretically and mathematically, if you invested 50% of your income each month/year, received 5% net rate of return, and did not increase your expenses after you retire outside of inflation, you could retire after 17 years of working1. How does that sound? Instead of working forty or more years, like most people, you could work less than half that.

Numero Tres – Slacker Budget

Truth be told, this isn’t even really a budget. All it really is doing is monitoring and tracking the amount of expenditure you have, the amount of gross and net income you make. Then, whether you are in the red or in the black (technically in the green on this spreadsheet) for the month. This report also is tracking your wealth balances and your debt balances each month so you know what progress you are making in your net worth (which will improve if you are not spending more than you should and using the amounts you should towards getting rid of debt and investing). Finally, it gives you a year end breakdown of total income, total expenditure, total gain or loss (net) of the difference between the two.

If you want to do the slacker option, see this picture and structure your “budget” just like this in Excel.

I did you the favor of plugging in example lines and columns for you to use. You can just duplicate the example with your actual numbers.

On the last day of each month, you need to go into your bank account and plug in the total income that came into it (your “Net Income” on the sheet) and then add up the expenses from the month and plug in that total next to “Monthly Expenses”. I also plug in my gross income each month (before deductions and deposits into my bank account) so I can plan for taxes. If you spent less than you made, you plug in the amount you didn’t spend in the “Gain/Loss Net” column for the month and mark it green. If you spent more than you made, you plug in the amount of overage in the “Gain/Loss Net” column and mark it red. This makes things very transparent. You are either a good boy or girl, or bad. At the end of the year you can see/add up your total and see if you are green or red.

You also plug in the current balances of all investment accounts, savings accounts, your estimate home value (if applicable), each month. Then, also, plug in the total of the debt balances you have below that. You can then see how your net worth is growing (net worth is below the asset and debt columns because you subtract your debt balances from your total assets – including home value – to come to that figure). Just a reminder, net worth can be positive or negative in balances also. If you have a negative net worth, I’d recommend marking that balance red also so you psychologically want to change it.

After months of tracking this information (EVERY MONTH AT THE END OF THE MONTH – PUT IT IN YOUR CALENDAR), you will see noticeable changes in your financial outlook. Seeing things such as your net worth improve, your spending decrease to be in range, your investments growing, and more, can have great psychological benefits. You will see you will become more hopeful with your finances, and even more eager to grow your net worth faster. This will come with any of these budgeting techniques, so just make sure you pick one and monitor it every week or so.

All I want is for you to become financially strong, followed eventually by financially free. Budgeting is of major importance to get you there.

For another helpful idea, one way to help yourself look forward to completing your budget planning moving forward is to reward yourself at certain milestones. If you have completed your budget for 3 months straight, 6 months straight, 9 months straight and so on, give yourself rewards or presents for doing so. Yes, that might affect your budget, but not really if you budget those rewards in, right? If you do track your net worth, maybe getting to certain net worth figures ($50,000 net worth, $100,000 net worth, $250,000, etc.) also should deserve a reward. Think of ways to encourage yourself to continue to do good with your money. Part of the trip is the ride, enjoy it.

Want a quick chart on how long you have to work (in years) based on what percentage of your income you save? Here you go.

Oh yeah, plus here is a completely random picture, just because it is cool. Your welcome.

0 Comments