31 Oct 2024

Post by Midwest Money Mentor

Just in case you were wondering, yes I type in Spanish (because Goggle Translate showed me how). What does that beautiful Spanish sentence above mean? Of course it means Sexy Finance Notes. You are welcome. Notas de finanzas Sexys. Make sure you try to say it like three times in an Antonio Banderas’ accent, preferably to your spouse or significant other.

In this series (the Notas de finanzas sexys series) we discuss other important aspects you need to mentally grasp to make sure you are truly making large jumps in your financial goals. See, the sexy series title makes all the sense now, right? With this particular post, we are going to deep dive into how buying vehicles that are “So Hot Right Now” can have large impacts to your wealth

Lets start by saying, I drive a hailed out 2008 Honda Ridgeline, that I bought for $3500 (thirty five hundred, not thirty five thousand) with a salvaged title and 140,000 miles, and I freaking love it.

My love of this vehicle comes for multiple reasons:

- It is actually fairly nice. It has leather seats, a Bose speaker system, a sunroof, ample seating, hidden and creative storage compartments, and it is a Honda, so it hopefully will last forever.

- I SAVE SOOO MUCH FREAKING MONEY BY DRIVING IT!!!!!! Holy crap. I paid cash for it (it was $3500 after all), so I have no car payment and therefore pay no interest costs. My insurance is like $500 (a year!) because it is an old Honda (parts galore available).

- And, it is a truck (not the prototypical “manly” truck, but still a truck) so hauling trash, yard waste, material from remodels on my investment properties, etc. can all be done with this vehicle (I don’t need another). And it gets through snow, mountain trails, and so on, no problem. The only negative is the gas mileage isn’t that great, but that is what we use my wife’s car for (which also is cheaply purchased).

You might think I am weird for being so excited about owning a old, kind of crappy looking (on the outside) vehicle, but you need to understand how much faster owning this vehicle has moved my family towards financial freedom. I would take a wild guess that putting the 30,000 to 50,000 worth of payments that many other people are making on their vehicle purchases would have slowed my family down by probably 7 years on our financial freedom journey.

If you are a car guy or gall, that is fine. But having the ability to be able to retire 7 years earlier just because I didn’t drive a brand-new car around is A-OK with me. I like the freedom of the road, but not as much as the freedom from debt and the freedom to work when I want to.

Outside of my entirely biased opinion about driving a cheap car, let’s go to some studies to shed some light on this conversation.

To own a new car, or to not own a new car, that is the question.

First, let us start with one of the more famous studies out there on the topic of money. This study was summarized and broken down by the follow up book called “The Millionaire Next Door: The Surprising Secrets of America’s Wealthy1.

This book is very enlightening and will be sourced often during the different posts that are created on the Midwest Money Mentor blog. But, to keep it simple, let us highlight some of the notes from the book on this particular topic.

- Quote – “we discovered something odd. Many people who live in expensive homes and drive luxury cars do not actually have much wealth. Then we discovered something even odder; Many people who have a great deal of wealth do not even live in upscale neighborhoods”.

- Quote – “Only a minority (23.5%) of us (millionaires) drive the current-model-year automobile. Only a minority (19%) ever lease our motor vehicles”. – This means that 76.5% of the millionaires (their study showed) drove older cars (not new vehicles) and 81% purchase the vehicle and don’t lease it.

I don’t know about you, but those specific conclusions from the book:

- That many people who display wealth often have very little wealth and are not millionaires.

- And a large majority of millionaires do not drive new model year vehicles.

is fairly interesting. What it seems to be telling us is that those who gain their financial freedom do so by purchasing personal items for low cost and for utility, not status. They do not buy cars, for instance, that have a large price tag or that hopefully make that person look cool for a bit.

Scandalous information.

But, numbers wise, what does that mean?

Let us look at a few different examples. I am going to compare the estimated 5 year costs of car ownership using our online, friendly calculator supplied by Edmonds.com2.

We will look at the purchase of a brand new Ford Bronco (which people are buying like freaking crazy, currently), to a 2018 Ford F150, to my old Honda Ridgeline. All Vehicles are suvs or trucks with not terrible to even good ranges of ability to get through winter weather, etc. All costs are based on my local area code (57701), and financing and costs established by Edmonds.

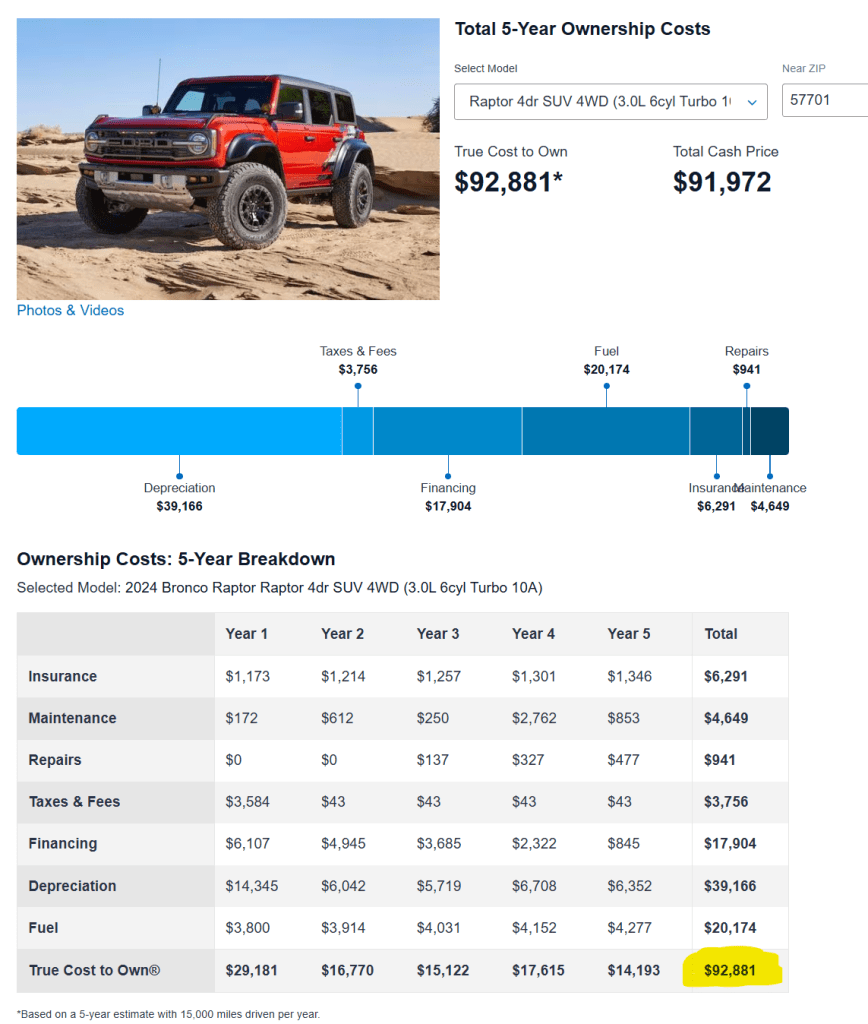

Here is the first cost to own calculator, on the “so hot right now” Bronco. Notice the 5 year estimated, total price tag at the top and bottom.

Just for the record, I have bought homes (rental properties) for far less than $92,881. And those are making me money every month, not costing me money.

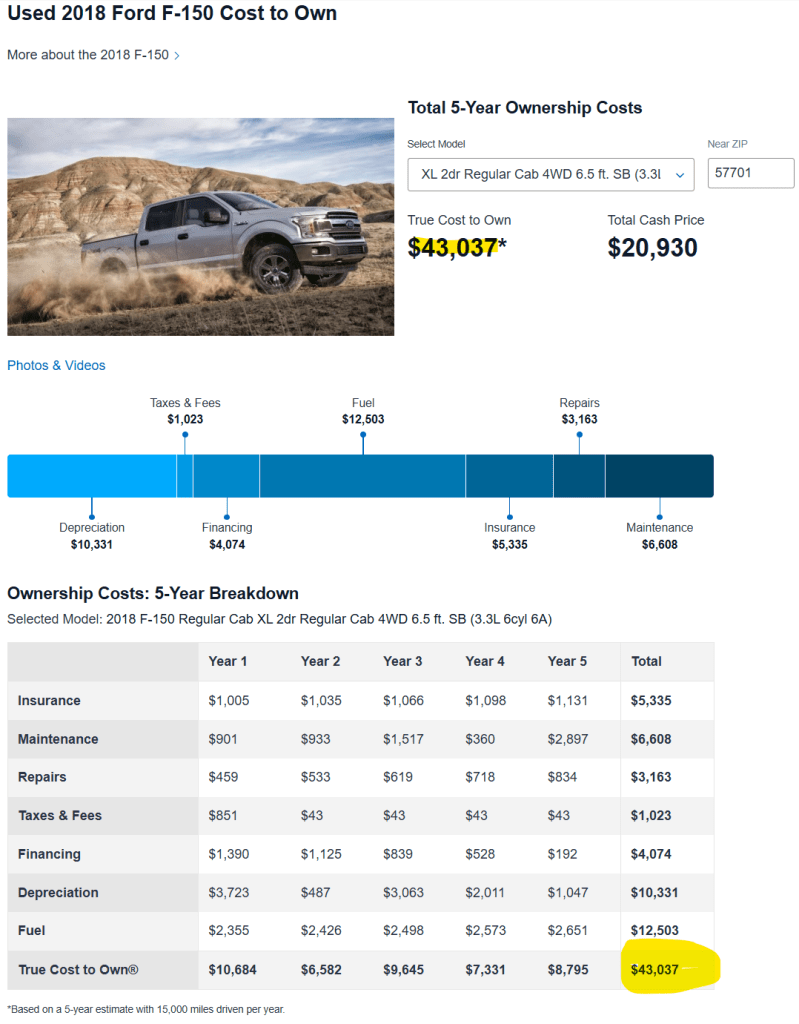

How about if we jump to the 5 year old F150?

Notice, that little over 5 year difference on a not as hot right now truck drops the anticipated costs of ownership by ALMOST $50,000 in that 5 year period! I mean, take that into your brain mush, please. If you invested that $50,000 savings over that 5 year period, at a gross average return of 7%, and then let it sit invested for 20 years, that would grow to over $230,000. So, in other words, taking the money you didn’t spend on the brand new, so hot right now, vehicle and investing it (and only it, no other amounts) could accrue you $230,000, which is more investment dollars than most Americans have. This one savings scenario, that is it. What if you did this multiple times over the years (because I’m assuming you will have to get a different car at some point in the future as well).

Finally, let us compare my car next. Sadly, my car is too old for Edmonds.com calculator to figure out. So, we will just do some manual math.

- Insurance costs – Looks like Edmonds is using an example of insurance increasing around 3% a year. I’ll do apples to apples numbers per year then, also. My current vehicle insurance, though, is $498 a year (yeah cheap vehicles!). So, year one – $498.00, year 2 -$512.94, year 3- $528.33, year 4 – $544.18, and year 5 – $560.50. Total that equals $2643.95.

- Maintenance – I’m going to use maintenance that is similar, but a little above, the F150 because the F150 shows as higher than the Bronco and because I am not sure my yearly costs, exactly. So let’s just play it safe and estimate higher. We will use $7,000 total.

- Repairs- I have been very lucky and have had very little repairs despite my vehicle being a 2008. So, even though I have probably had $2500 of total repairs in the last 5 years, let us play it safe again and say my next 5 years will be much higher. Let us use $1200 a year, or $6000 total (almost twice as high as the F150 example).

- Taxes – I bought it for $3500, so my up front taxes were like $210, plus we will use the same annual amounts show above (in both examples) for this area. Total for everything equals $425.

- Financing – $0. I bought it in cash.

- Depreciation – Guys, it already was only worth $3500. Lets say it depreciates in half, which is probably unlikely. But, total – $1750.

- The calculator does not explain how they are calculating the gas costs, outside of driving 15,000 miles. But, some backwards math tells me they are using somewhere around $3.45 per gallon for their cost example. If I do the same with my ridgeline (which gets around 20 miles per gallon), the first year would be around $2587.5, with each year after going up 3% (like the insurance). Second year would be – $2,665.13, third year – $2,745.08, fourth year – $2,827.43, and fifth – $2,912.26. For a total of – $13,737.39. By the way, I actually drive way less miles than this, but we are doing apples to apples, FOR SCIENCE!

My total 5 year costs would then be $31,556.34 in this example. That is a full $61,324 of savings over that 5 years compared to the Bronco. Same equation of leaving that with a 7% return for 20 years, would create $283,000 extra in investments for me. And that is including me driving $15,000 miles a year and having $13,000 combined maintenance and repairs in the next 5 years. The miles are definitely higher than I will do, and hopefully the repairs and maintenance are high also. So my savings is could be much more.

Want to invest more and retire early? Don’t spend your hard earned money on new or fancy cars. Hopefully I made my point?

0 Comments